Recent News

Cash, Check, or Card: How DSD Payment Habits Are Quietly Shifting in 2026

A route driver finishes a stop, confirms the delivery, and then comes the familiar question: how is the customer paying today?

Maybe it's cash from the register. Maybe it's a paper check that needs to be collected, deposited, reconciled, and eventually cleared. Or maybe, more often than a few years ago, the customer asks, "Can I just put it on a card?"

That small moment at the stop says a lot about where DSD payments are heading.

Direct store delivery has always had its own rhythm. Drivers aren't just dropping product and moving on. They're collecting payments, handling paperwork, managing credits, confirming invoices, and helping keep the account current. For many distributors, cash and checks are still very much part of the daily route process.

But the payment mix is changing. Not all at once, not across every customer, and certainly not in a way that makes DSD "cashless." The shift is quieter than that. It happens one account at a time — when a retailer asks for an easier way to pay, when a distributor wants fewer collection issues, or when the end-of-day settlement process starts taking more time than it should.

In 2026, the question isn't whether cash and checks still matter in DSD. They do. The better question is whether distributors are ready for a payment mix that's slowly becoming more digital.

The Check Is Still on the Truck, But It's Fading

In many industries, paper checks already feel like yesterday's payment method. In DSD, they're still a familiar part of the route.

That makes sense. Route distribution has always been relationship-driven and stop-based. A driver walks into a store, delivers product, prints or confirms an invoice, and collects payment while they're there. For independent retailers and smaller accounts, that process may have been built around cash or checks for years.

But the broader B2B payment trend is clear, and the long view is striking. The Association for Financial Professionals has tracked check usage for two decades: in 2004, checks accounted for 81% of B2B payments, and by 2025, that share had fallen to just 26%. Nacha, the organization behind the U.S. ACH network, cites this data as evidence of how quickly checks are receding in business-to-business payments.

That doesn't mean DSD distributors should expect checks to disappear overnight. They won't. Many independent retailers still use them, and some accounts may prefer them for years to come.

But it does mean the rest of the business world is moving faster than the truck. For DSD operators, that creates a practical tension: the route still needs to support cash and checks, but it also needs to be ready when more customers want to pay by card or through a more automated process.

Why Retailers Are Asking to Pay by Card

The push toward card payments isn't only coming from distributors. Increasingly, it's coming from customers.

Independent retailers, c-store owners, and small account operators are consumers, too. They pay bills online. They tap cards at checkout. They manage banking from their phones. They're used to digital receipts, cleaner records, and fewer trips to the bank. So when they look at a DSD invoice, it's not surprising that some of them want the same convenience.

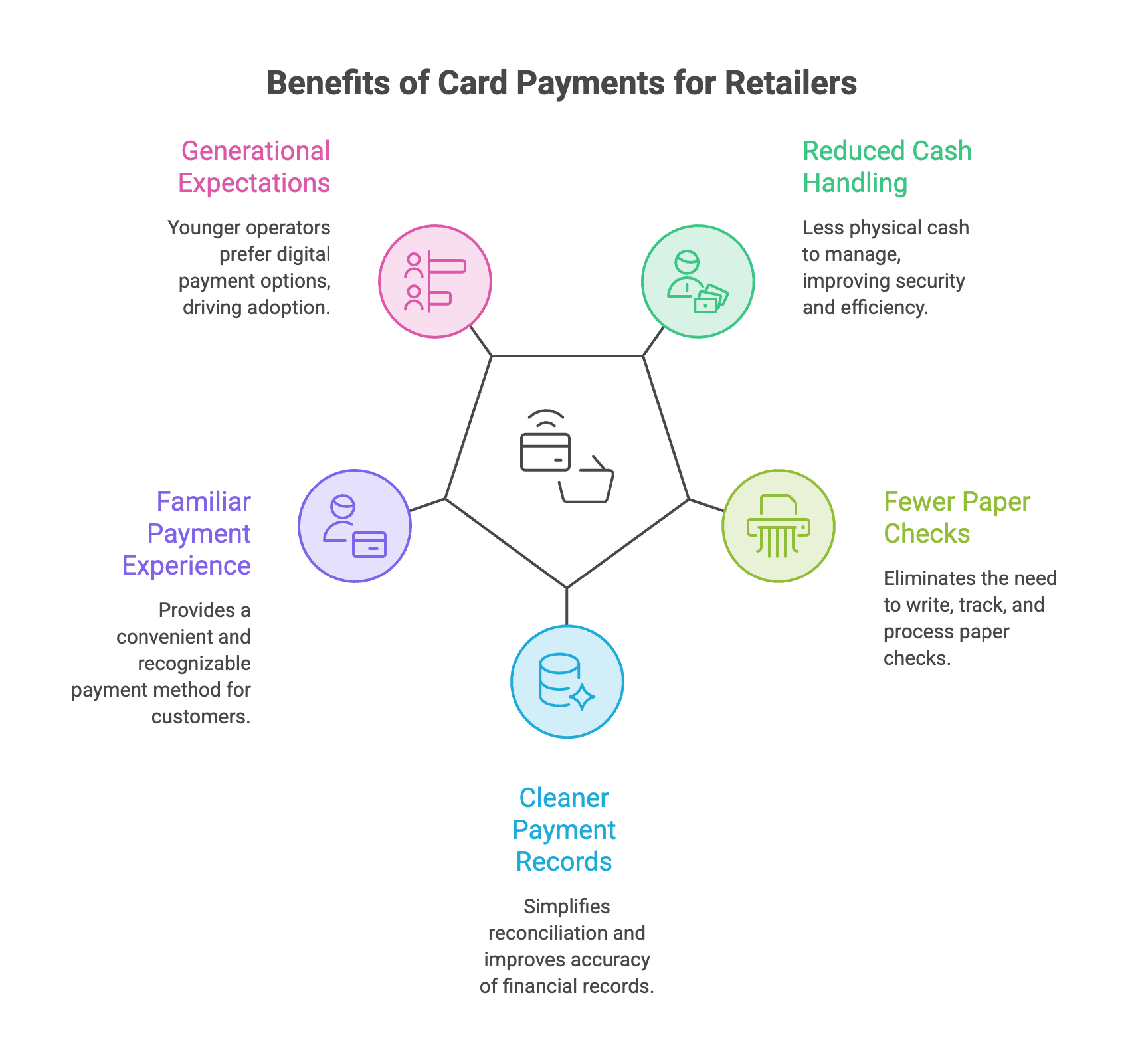

For a retailer, paying by card can mean:

- Less cash handling at the store

- Fewer paper checks to write and track

- Cleaner payment records and easier reconciliation

- A more familiar payment experience

There's also a generational factor. As younger operators take over stores, routes, and family businesses, expectations change. They may not see paper checks as the default method for settling a business invoice. They may simply expect the option to pay by card, store a payment method, or eventually pay through a portal. These shifts mirror the broader move away from checks toward faster, more familiar digital payment methods happening across B2B.

At IntegraSys, we've seen this shift show up in the conversations distributors are having. More requests are coming in for credit card payment options, not because every customer wants to change, but because enough customers are asking that distributors are paying attention. This isn't just a software trend. It's a customer-service trend.

What Cards Actually Fix for the Distributor

For distributors, card payments aren't just about giving customers another option. They can also solve real operational problems.

The most obvious benefit is faster payment. When invoices sit open, the cost isn't only financial. Someone has to follow up. Someone has to track what's outstanding. Someone has to reconcile what was collected, what was missed, and what still needs attention. Card payments can reduce that friction.

They can also reduce the amount of cash on the truck, which matters for safety, accountability, and end-of-day settlement. Cash has to be counted. Checks have to be handled. Payments must match invoices, and exceptions must be investigated. The more manual the process, the more time it takes and the more room there is for mistakes.

For many distributors, the fee question is the biggest objection. That's understandable. A 2–3% processing cost is easy to see — it shows up directly. But the cost of slow payment is often harder to measure. It shows up in collection calls, delayed cash flow, bank trips, manual reconciliation, returned checks, and staff time spent chasing money that should already be in the account.

The right way to evaluate card payments isn't simply "fee or no fee." It's a tradeoff:

- What's the cost of waiting?

- What's the cost of chasing?

- What's the cost of cash handling?

- What's the value of getting invoices closed faster and cleaner?

For some accounts, cash or check may still make the most sense. For others — especially customers who want a more convenient way to pay — card payments can be a practical improvement for both sides.

Making the Shift Without Friction

The challenge for DSD distributors isn't just accepting cards. It's accepting them in a way that fits the route. Payments need to connect back to invoices, settlement, customer accounts, and the daily workflow. A disconnected card process can create almost as much work as it solves.

That's why IntegraSys works with Authorized Credit Card Systems (ACCS), a processing partner that integrates with DSD Manager. Today, that integration runs through a credit card authorization setup: customers complete a form granting permission for their card to be charged automatically — monthly, or on another agreed-upon schedule — for all open invoices. Once the payment is processed, those invoices are marked as paid in DSD Manager.

That gives distributors a practical way to support card payments without turning the route process upside down. The benefits include competitive transaction fees, no large monthly platform costs, less manual follow-up on open invoices, and cleaner payment posting in DSD Manager. ACCS also handles PCI compliance — the security standard major card companies use to protect cardholder data — which matters because accepting cards introduces real data-handling responsibilities.

Looking ahead, there are deeper integrations on the roadmap. That could include allowing customers to select specific invoices to pay via a web portal or directly in the Route Manager mobile app. The goal isn't to force every customer into one payment method. It's to make payment easier, cleaner, and better connected to the route, whether the customer pays in cash, by check, or by card.

Conclusion

At the end of the stop, the driver still needs an answer. Cash? Check? Card?

For now, many DSD routes will continue to support all three, and that flexibility is part of serving independent retailers well. But the balance is changing. As more customers ask for card options, and as distributors look for ways to reduce collection friction, payments are becoming a bigger part of the customer experience.

The distributors who notice the shift early will be better prepared to protect cash flow, simplify settlement, and meet customers where they already are. Because in DSD, getting the order delivered is only part of the job. Getting paid cleanly, quickly, and with less friction is becoming just as important.

Streamline Your DSD

.jpg)

All Rights Reserved.